Chart of the Month

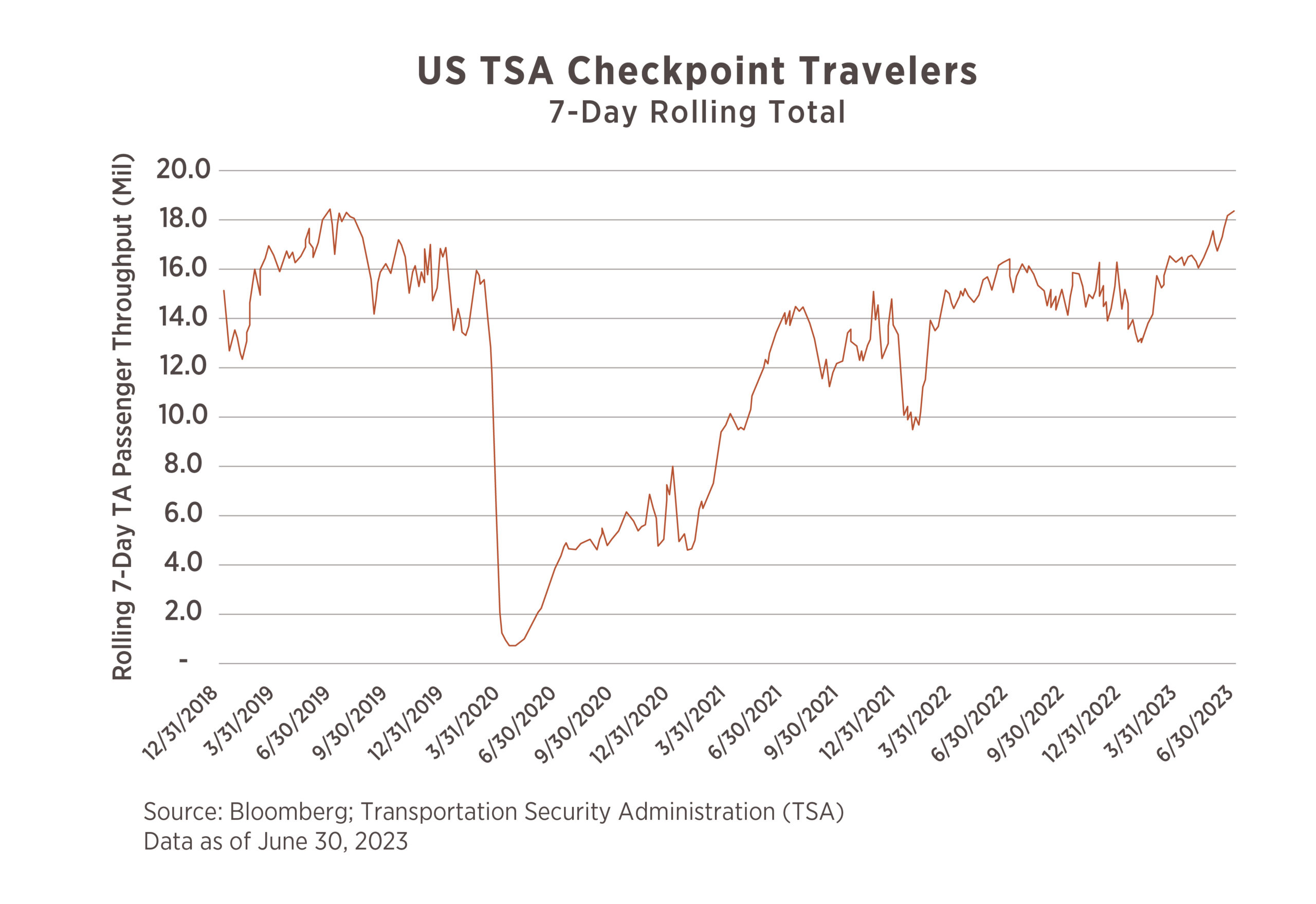

Up, Up, and Away – at least that is what the US consumer is back to doing! The US TSA started producing a daily number in 2019 to show the number of passengers going through checkpoints. June 30th,2023 was a new daily record at 2,884,683 passengers and the 7-days ending on 6/30/23 was also the largest 7-day total since they started tracking. See chart above. What this shows is travel is essentially back to where it left off prior to the pandemic. With the US Consumer being the engine of the US economy (~70% of GDP), this could be an indicator (amongst many) to keep an eye on.

With unemployment remaining near record lows and a high ratio of job openings to job seekers, perhaps the fear of an imminent economic threat is still not out there yet for the average person. It could also be, however, that people just can’t possibly stand not to take a trip after being unable to for such a long time! There are other sources of information suggesting that consumers are becoming more stretched as delinquencies on auto loans and credit cards continue to inch higher. And this is even before many borrowers will be set to resume student loan payments following the Supreme Court’s strike-down of the Biden Administrations Forgiveness Plan.

So while airport traffic may look robust today, it could be something to watch as an early indication the consumer is beginning to feel stretched. If so, beware of turbulent times ahead!

As a parent, you’ve probably thought about how to teach your child financial literacy. Nobody wants their children to be dependent on them forever, so it is important they have a solid understanding of how to make and save money. Though every family’s financial situation is very different, there are some tips every parent can use as a jumping off point when raising financially independent children.

Talk about money early and often

It may go without saying, but when starting to talk to children about money, it’s important to ensure the conversations align with their age. The whole goal here is to support your children in developing a healthy relationship with money. A good time to start talking about money with your kids is around the same time they begin to develop math skills – for some this is second grade and for other kids this may be earlier.

Money shouldn’t be a one-time conversation topic. Rather, it should be an ongoing subject of discussion. The hope is that your children will begin to feel comfortable discussing finances and will become interested in learning more. If you want professional advice, a simple Google search will reveal countless books for educating kids about money.

Model responsible money habits

Your kids look to you as a model for just about everything in their formative years, and managing money is no exception. A large part of teaching kids good financial habits is making sure you’re modeling them yourself. Talk about the expectations and “norms” around money in your family, lead by example. Here are some ways to do that:

- Make a list before heading to the store and set a budget. Even if you don’t “need” to set a budget, this practice can teach kids to stick to the list and only buy what they need.

- Talk openly about saving money for new things such as vacations, a new car, house, college funds and retirement.

- If something breaks, show your kids how to fix it instead of throwing it away and buying a new one.

- Avoid “retail therapy” or shopping with the goal of cheering yourself up.

- Set waiting periods to guard against impulsive purchases. Are you still thinking about buying those shoes a week or two later?

Allowance

As long as your child can do basic math, an allowance can be incorporated to help introduce them to responsible saving and spending. The amount you give your child is up to you, but any amount can be a great way to teach kids money basics.

It’s vital though to have some kind of behavior tied to receiving the allowance. There are birthdays and holidays but for a regular weekly allowance, what are you requiring of your child? This could include household chores or academic achievement. Whatever behavior you choose to tie to their allowance should be clearly laid out and discussed.

Spending, saving, and values

After setting an allowance, it is inevitable that your child will begin to voice how they want to spend their money. Now, you can once again model good financial reasoning. If your child wants to spend each allowance immediately and realizes they don’t have enough to buy a large-ticket item, you can remind them of a time you were also saving for a larger purchase. Maybe it took some hard work and patience, but eventually, you could afford the item.

Let mistakes happen

Your child will make financial mistakes – that’s part of the learning process. It will be tempting to take over more control when mistakes happen especially costly ones – but it’s vital to give kids room to test out certain behaviors and learn from the consequences. It is arguably better for the mistakes to happen at a young age, because your children can learn from them sooner. It is much worse, however, if these financial missteps occur when your children are independent.