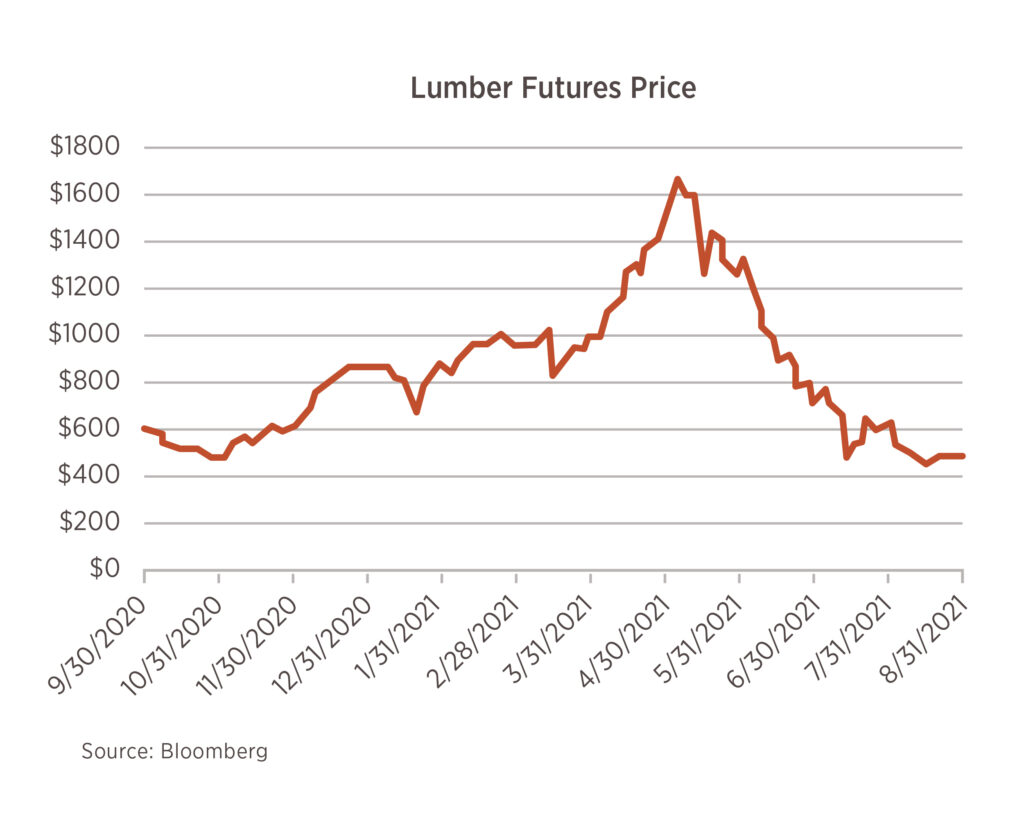

Chart of the Month

Earlier this year, the phenomenon of rising lumber prices was often pointed to as a sign of inflationary price pressures. It was certainly drastic to see the price triple from the date of the first effective vaccine announcement in November 2020 through April of this year. Since April, however, that entire price increase has been reversed. While the decline may be partially due to decelerating growth and additional virus concerns, it also reflects a supply and demand response. High prices incentivize additional production. While other industrial commodities such as copper and oil have also declined in price since April, lumber stands out for both the scale of its climb and the magnitude of its fall.

Qualified Charitable Distributions

A choice for I.R.A. owners who want to reduce taxes linked to I.R.A. distributions.

Do you have an I.R.A.? As you enter your 70s, you may start to look at that I.R.A. not only as an asset, but also as a problem. By law, you must take required minimum distributions (R.M.D.s) from a Traditional I.R.A. once you reach age 72; there are very few exceptions to this. The downside of these R.M.D.s? The entire distribution is taxable. (You never have to take R.M.D.s from a Roth I.R.A., provided you are its original owner.)1

While the income from the R.M.D. is nice, the linked taxes can be a headache. Relief for that headache might be available to you, though. Did you know that you can potentially satisfy some or all of your annual R.M.D. requirement in a way that can help you manage taxes and make a charitable impact?

Consider the Qualified Charitable Distribution, Q.C.D. This is a direct asset transfer from an I.R.A. to a charity or non-profit organization of your choice. The organization must be tax-exempt under Internal Revenue Section 501(c)(3).2

A Q.C.D., sometimes called a charitable I.R.A. gift, is intended to accomplish two things. One, it gives you a chance to contribute up to $100,000 in a single year to a cause or charity. Two, you can count the entire amount of the Q.C.D. toward your R.M.D. for the year, and the Q.C.D. amount may not be included in your gross income.2

You must be at least 70½ years old to make a Q.C.D. You may want to coordinate a Q.C.D. with the help and guidance of a financial professional, because if you improperly manage the transfer of assets between your I.R.A. and the charity, the tax break you hope for could be lost. You also need to allow enough time for the asset transfer to occur, meaning Q.C.D.s are best arranged before the very end of a calendar year.2,3

In 2020, the age limit for putting money into a Traditional I.R.A. was lifted, and some older I.R.A. owners wondered if they could make a Q.C.D. to a charity and simultaneously characterize it as an I.R.A. contribution. The Internal Revenue Service said no to that.2

That said, a Q.C.D. is a choice that you may want to look at, especially if you think of taxes when you think of your mandatory annual I.R.A. distributions. It should be noted that the tax treatment of I.R.A.s can change from year to year, and remember, this article is for informational purposes only and does not constitute real-life advice. If a Q.C.D. interests you, consider talking with a financial professional before making any move.