“Double” – a commonly used word across various settings such as:

- The Rule of 72: Shortcut to calculate the time it takes to double an investment

- “Double or Nothing”: Risk it all for a higher payout

- A baseball “double”: Reaching 2nd Base

- “Double Take”: Looking twice in surprise

- “Two-for-one”: A bargain shopper’s dream

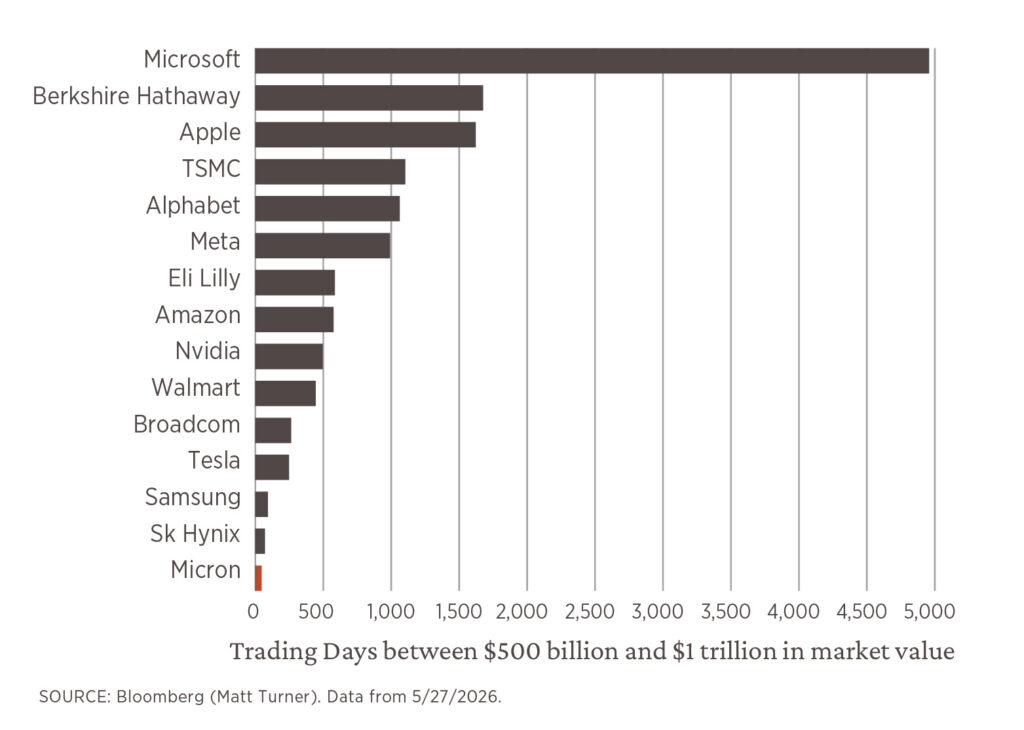

This month’s chart focuses on “doubling” differently, capturing a recent event that occurred at unprecedented speed. It shows a list of today’s largest global companies and the time it took for their market value to increase from $500 billion to $1 trillion. What stands out is the meteoric rise of the bottom three – Samsung, SK Hynix, and Micron1 – which achieved this milestone far more quickly than the companies before them. Notably, all three reached this milestone within the month of May. According to the data, it took just 48 trading days for Micron, 61 for SK Hynix, and 82 for Samsung.1

These three companies all share a common theme: exposure to the AI-driven demand cycle and a product set focused on memory. It is no coincidence that all have achieved this recent success in a similar fashion. Historically, the memory product business has been highly cyclical, based on the ebbs and flows of end-market demand. At present, however, the insatiable appetite for building out AI infrastructure has created a surge in near-term profit expectations.

Despite this recent move in a few stocks being eye-catching, especially given their already large size, doubling an investment is typically a longer-term process. One way to frame this is through the “Rule of 72”, a simple estimate on how long it takes an investment to double based on its expected annual return. For example: 72 / 6% = 12 years. Thus, an investment earning 6% annually will take 12 years to double in value.

Short bursts of rapid growth can occur, particularly in a highly concentrated setting. However, sustained wealth creation and preservation is more often driven by consistent compounding over time.

1. Clark, A., & Hamilton, A. (2026, May 27). The ‘Insatiable’ Logic Behind Micron’s ‘Extreme’ Gains. Barron’s.

Level 1: Must Haves

Goal: Plan for and document the transfer of assets per your wishes with minimized transfer costs.

- Last Will and Testament: A will specifically spells out how you want your assets distributed and appoints guardians for any minor children.

- Living Trust: A living trust avoids probate, allows for privacy, and designates how assets are to be divided upon your death.

- Healthcare Power of Attorney: Designate an agent to make your healthcare decisions in the event you are unable to make them while you are living.

- Financial/Property Power of Attorney: Designate an agent to make financial decisions if you are unable to make them while you are living.

- Review Co-ownership Provisions and Account Titling: Correct ownership and account titling ensure assets and accounts pass the way you intend.

- Periodically Review Beneficiary Designations: This is important as some assets (such as IRAs, Life Insurance, and Annuities) pass to your designated beneficiaries.

Upon life events (marriage, divorce, birth, adoption, etc.), review these aspects of your estate plan to ensure all information is up-to-date.

Level 2: Considerations

Goal: Further enhance the direction of assets, minimize estate taxes, or increase asset protection.

- Grantor Retained Annuity Trusts: Grantor Retained Annuity Trusts (GRAT) seek to pass assets to beneficiaries free of estate and gift tax that have appreciated over the IRS Section 7520 interest rate.

- Charitable Options: Explore charitable giving options, such as Charitable Trusts, Donor-Advised Funds, and Foundations, for both philanthropic and tax benefits.

- Irrevocable Life Insurance Trust: Because life insurance is not necessarily estate tax-free, consider establishing an Irrevocable Life Insurance Trust.

- Qualified Personal Residence Trust: A Qualified Personal Residence Trust (QPRT) is a type of trust that allows its creator to remove a personal home from his or her estate.

- Spousal Lifetime Access Trusts: Spousal Lifetime Access Trusts (SLATs) allow spouses to pass assets to each other and other loved ones free of estate and gift tax while maintaining limited, indirect access to the assets.

- Intra-Family Loans: Intra-Family Loans can provide family members with lower borrowing rates than traditional financing options.

- Special Needs Trusts: A Special Needs Trust preserves a beneficiary’s eligibility for needs-based government benefits.

Level 3: Advanced

Goal: Consider options for complex estate tax issues or liability concerns.

- Self-Cancelling Notes: Self-Cancelling Notes allow the exchange of property for periodic payments based upon mortality.

- Trust-Friendly Jurisdictions: Certain states, including Delaware, have favorable trust statutes, offering the potential to pass assets across generations without incurring transfer taxes (Dynasty Trusts), delegate responsibilities to non-trustees (Directed Trusts), protect assets, and more.

- Family LLPs and LLCs: Family Limited Liability Partnerships and LLCs provide legal, financial, and tax structure to family businesses.

What is portability?

Portability allows you to use your spouse’s unused estate tax exclusion. While portability was made permanent for federal estate tax purposes, you should check if your resident state also allows for portability of a deceased spouse’s unused estate exclusion. In the event your resident state does not allow for portability, it may make sense for both spouses to have assets in their respective names (or a trust’s name) up to the resident state’s estate exclusion amount.

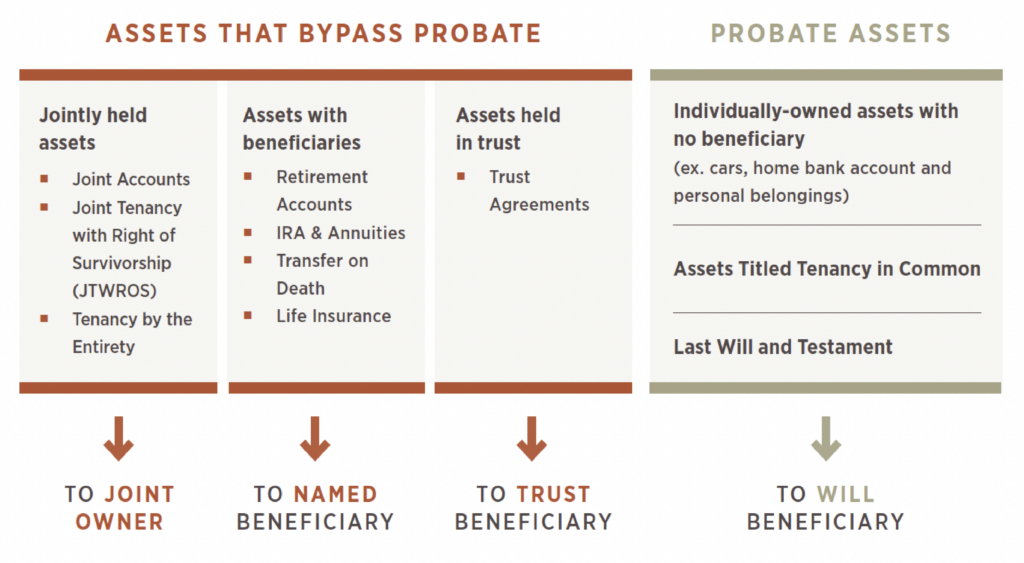

How Assets Pass Upon Death

Probate vs Non-Probate Assets

Probate is a public court process that helps settle legal and financial matters upon death according to a will, if written.

Court costs, length of time, the lack of privacy, and family disagreements are all potential issues that may arise within the probate process. With proper estate planning, you can limit the amount of assets that pass through probate.

Digital Assets

Nearly all 50 states have passed a version of the Revised Uniform Law Commission’s Fiduciary Access to Digital Assets Act that legally allows for an executor, trustee, etc., to access a deceased’s digital accounts. Consider discussing your digital estate with your attorney and the potential need to share online access information with your executor or trustee.

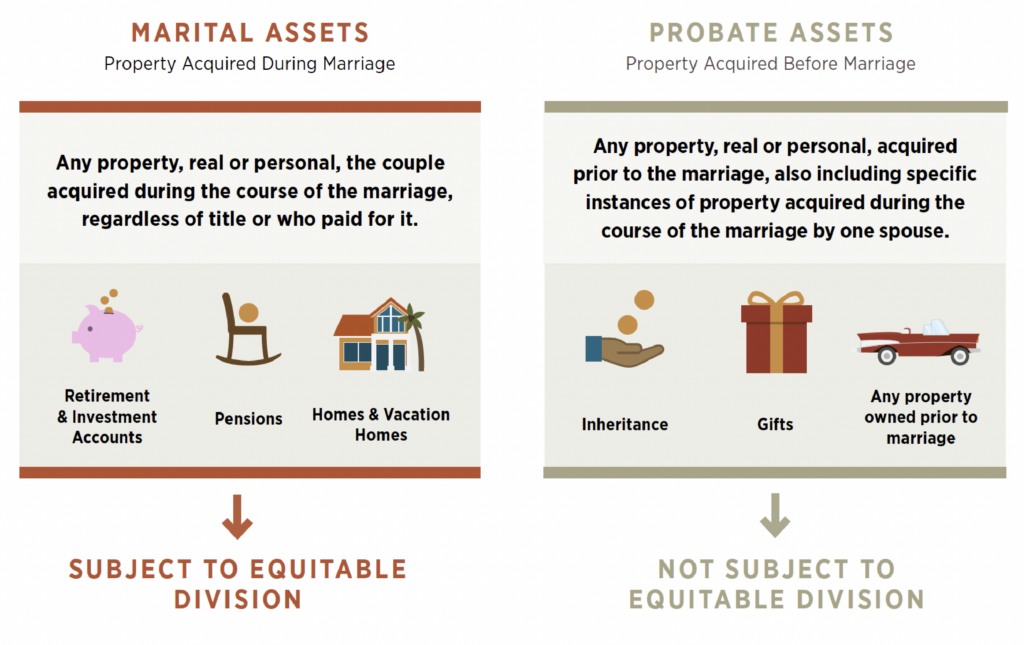

How Assets Pass Upon Divorce

Marital vs Non-Marital Assets

Estate planning is not divorce planning. Without a pre- or post-nuptial agreement, marital assets are subject to equitable division in a divorce proceeding.

Effective for divorces finalized after January 1, 2019, alimony payments will no longer be tax-deductible by the paying spouse and will not be added to the taxable income of the receiving spouse.

Tainting of Assets

Non-marital assets may be tainted during the course of a marriage and may be treated as marital assets in a divorce proceeding. For example, if a spouse deposits a personal inheritance into a joint account or uses income from an inheritance to support the couple’s lifestyle, this non-marital asset may be treated as a marital asset.

Estate Planning Updates

A Window of Opportunity

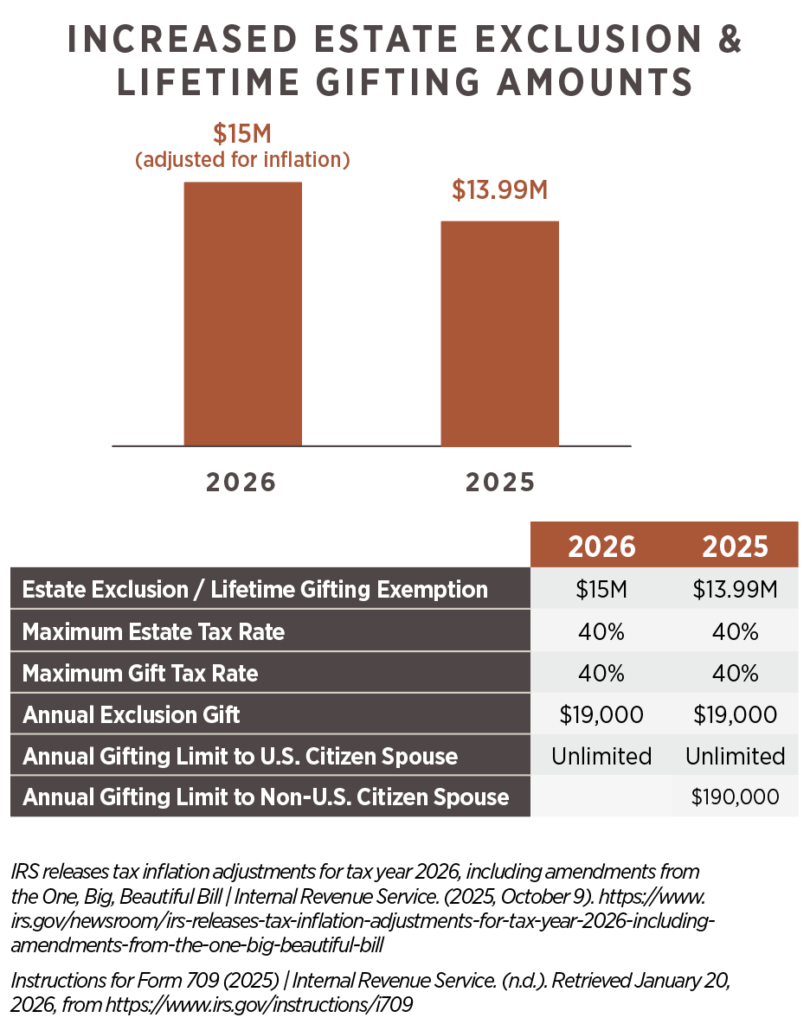

- The Tax Cuts and Jobs Act (TCJA) of 2017 significantly increased the estate exclusion amount (presently $15 million for 2026), which has helped HNW families plan and pass substantial assets to the next generation, tax-free.

- In July 2025, the One Big Beautiful Bill Act was signed into law, making many of the TCJA’s key provisions—most notably the enhanced lifetime gift and estate tax exemptions—largely permanent, providing long-term certainty for estate planning.

- The legislation also created a new tax-advantaged giving opportunity, allowing individuals to contribute up to $1,700 ($3,400 for married couples) to organizations that fund K–12 private school vouchers, with contributions fully offset by a federal tax credit.1

- Key Takeaway: Individuals who have, or are likely to have, a taxable estate and who have sufficient assets to fund expenses during their lifetime may want to consider gifting additional assets to loved ones now that the exemption is permanent.

Irrevocable Trusts

An irrevocable trust is a type of trust where its terms can’t be modified, amended, or terminated without the permission of the grantor’s named beneficiary or beneficiaries. These types of trusts have many applications but are typically used in planning for the preservation and distribution of an estate. Some specific uses may include:

- To take advantage of the estate tax exemption and remove taxable assets from the estate. Property transferred to an irrevocable living trust does not count toward the gross value of an estate.

- To prevent beneficiaries from misusing assets, the grantor can set conditions for distribution.

- To remove appreciable assets from the estate while still providing beneficiaries with a step-up basis in valuing the assets for tax purposes.

- To gift a principal residence to children under more favorable tax rules.

- To house a life insurance policy that would effectively remove the death proceeds from the estate.

Keep in mind, an irrevocable trust is a more complex legal arrangement than a revocable trust, mainly because of the tax implications. Be sure to seek a professional’s guidance when setting up an irrevocable trust.

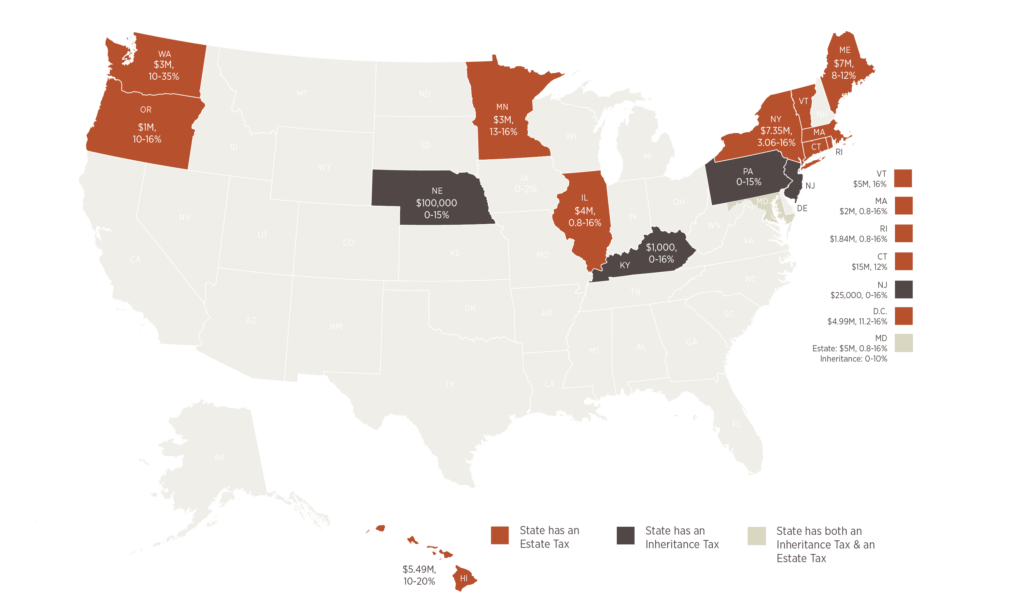

Don’t Forget Estate Tax at the State Level!

Many states have estate exclusions far below the federal level, which may result in state estate taxes. Older estate plans should be reviewed to ensure trust provisions incorporate current federal and state estate tax limits.

1. U.S. Bank. (2024, July 2). One big beautiful bill act: Key changes in the TCJA extension: U.S. bank. One Big Beautiful Bill Act: Key Changes in the TCJA Extension | U.S. Bank. https://www.usbank.com/wealthmanagement/financial-perspectives/financial-planning/the-real-impactof-the-tax-cuts-and-jobs-act.html