Chart of the Month

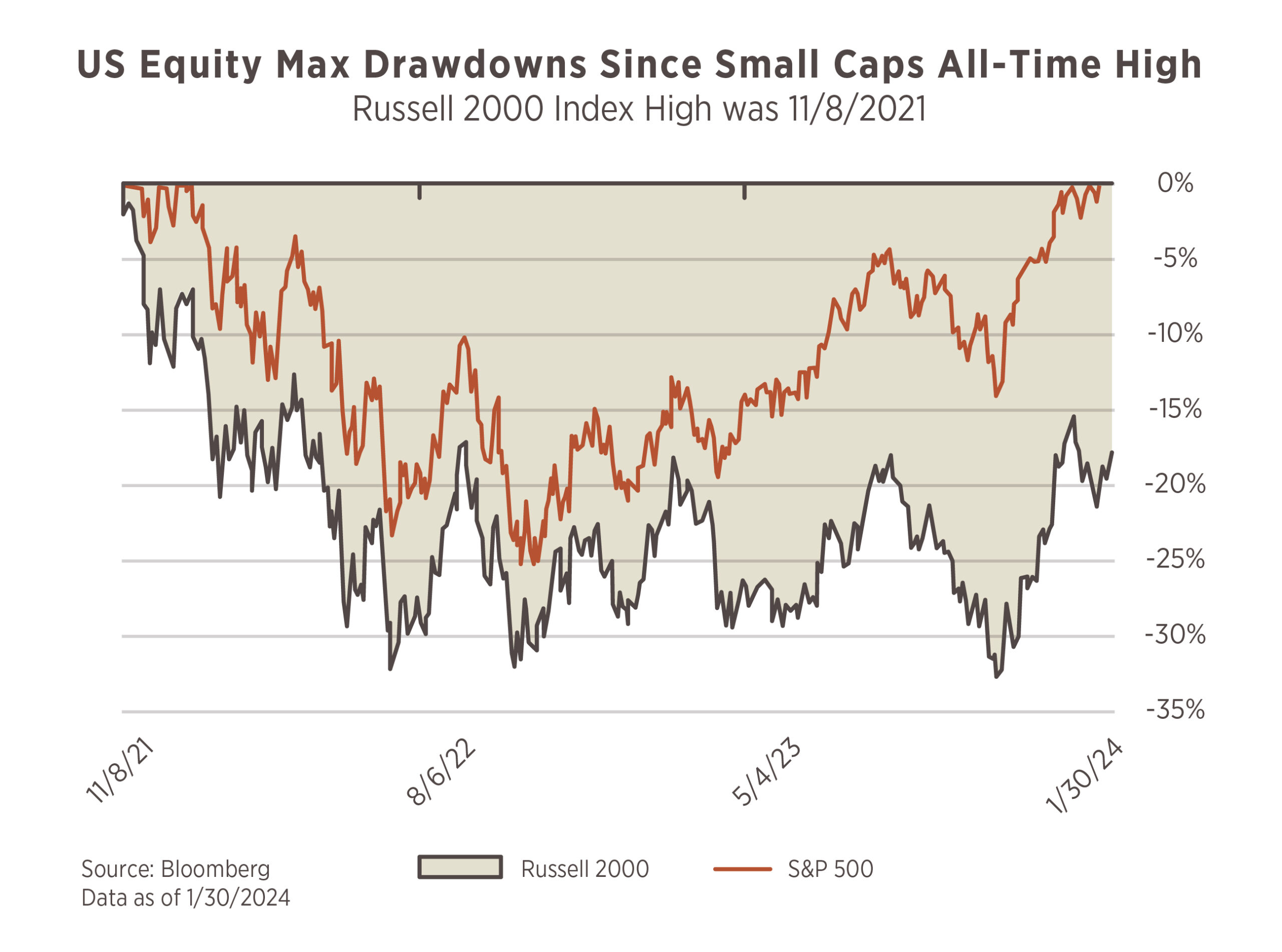

David vs. Goliath. The “Miracle on Ice.” Rocky vs. Ivan Drago. All are examples of the smaller prevailing. However, the chart we show this month has been the exact opposite: US Large Caps (S&P 500) achieved new highs in January 2024 while US Small Caps (Russell 2000) are still 18% below their record levels last seen in Nov. 2021!

As has been discussed almost ad nauseam over the past year, it is no secret that the S&P 500 was powered higher by the “Magnificent 7.” To understand how large the “Magnificent 7” has become, consider this. The Market Cap1 of those 7 companies – Microsoft, Apple, Alphabet (Google), Amazon, Nvidia, Meta (Facebook), and Tesla – is ~$12.7 trillion. The Market Cap of all ~2,000 companies in the Russell 2000 is ~$2.9 trillion. That means the 7 largest stocks are 4.3x the size of all US Small Caps. Perhaps even more interesting is that both Microsoft and Apple, on their own, are equivalent in size to the entire US Small Cap universe.

Two years ago, we wrote about the valuation gap between Small Caps (S&P 600) and Large Caps (S&P 500) earnings yields, reaching a point that had not been seen since the dot-com bubble in the late 1990s. Since we wrote that, not much has changed as that valuation gap has remained persistent and even slightly widened. In other words, US Small Caps continue to trade cheaper relative to US Large Caps. As the saying that is often repeated in sports goes: “They might be down, but they’re not out.”

The gap in performance between large and small companies is historically large and likely to be closed. As such, we think it is important for clients to discuss with their advisors having both large and small cap exposure in their portfolios.

1Market Cap refers to size the stock market attributes to each company; calculated as of 1/30/2024 from Bloomberg

If managing your personal finances feels like a daunting task, you are not alone. Only about 33% of Americans have some kind of written financial plan,i and in 2023 alone, financial illiteracy cost Americans an estimated $338 billion.ii

You may be asking yourself: “Where should I even start?” Here are some practical tips and strategies to help you begin to take control of your personal finances.

Retirement Planning

To many people, compound interest is considered the eighth wonder of the world. While that’s perhaps a bit hyperbolic, we do know that saving money early and often is foundational for a successful retirement.

Unfortunately, according to research, 57% of American workers save less than 10% of income,iii and nearly 56% of Americans surveyed are concerned that they will not be able to achieve a financially secure retirement.iv Below are some suggestions on how to better save for retirement:

- Maximize contributions ($23,000 + $7,500 age 50+ catch up in 2024)v to your company retirement plans (401k, 403b) and/or at a minimum, contribute enough to receive the full employer match.

- Consider backdoor Roth IRA contributions if your income level prevents you from making direct Roth IRA contributions. This is done by making a non-deductible contribution to a regular IRA and subsequently rolling it over into a Roth IRA. There are some IRS rules to follow, so we recommend speaking with a tax advisor or financial planner to ensure success.

- If self-employed, contribute to a Solo 401(k) ($69,000 in 2024)vi, SEP-IRA ($69,000 in 2024)vi or defined benefit plan.

- Work with a financial advisor to assess your current savings versus future spending needs; plan ahead and assume longevity. Online retirement projection tools exist that can also help with this analysis.vii

Income Tax Planning

Taxes can have a significant impact on wealth, investment returns and your long-term financial planning goals. While April is when most people file their tax returns, proper tax planning requires year-round attention. Here are some suggestions for doing so:

- Know the difference between your income tax bracket and your effective income tax rate (i.e., your tax rate inclusive of deductions, credits, etc.). Knowing the tax rate you actually pay can assist you in making better tax decisions related to items like the efficacy of making additional charitable contributions, the impact of a Roth conversion, or taking a part-time job in retirement. Tax filing software and/or your tax preparer can provide you with this comparison.

- Review the “asset location” of your investments to maximize after-tax returns and minimize unnecessary tax drag.

- Gift long-term appreciated securities rather than cash when making charitable contributions, as doing so will help avoid future capital gain taxes on the sale of those securities.

- If your income varies considerably year-over-year, ensure either safe harbor withholding amounts or make estimated tax payments during the year to avoid costly IRS underpayment penalties.

Estate Planning

Regardless of your level of wealth, having a proper plan in place is essential to ensure your family’s financial security after your death. Consider doing the following as soon as possible:

- Draft both wills and powers of attorney (financial and health) to not only direct your financial affairs at your passing or incapacitation but also to name guardians for minor children or other special asset bequests.

- Periodically review your estate plan documents to ensure alignment with your current situation and evolving state/federal limits.

- Evaluate estate taxes at the state level, as many states have estate exclusion amounts well below the federal level.viii

- Review your beneficiary designations at least annually and as your life circumstances evolve (e.g., children, divorce, increase in wealth, etc.).

- Consider more advanced planning techniques, such as gifting strategies, trusts and charitable vehicles, to help reduce estate tax liability prior to death.

Insurance Planning

Insurance is a tool to protect your assets, your income and your family. Policies can range from simple to the complex and are an important component to financial health. Here are some best practices:

- Review older life insurance policies for continued necessity or conversion options.

- Assess current property and casualty and umbrella policies, especially given changes in net worth or property values; look for gaps in liability coverage.

- Review health insurance and long-term care insurance to ensure proper coverage, terms and conditions and potential impacts on Medicare and Medicaid eligibility.

While the above is not a comprehensive list, simply tackling a few of these items today could go a long way towards successful future financial outcomes for you and your family. And you don’t have to go it alone. Please reach out to us for help, and we can collaborate with your accountant, attorney and other advisors to seek optimal investment, tax, estate planning and insurance strategies to accomplish your unique goals.

i Schwab 2023 Modern Wealth Index Survey, March 2023.

ii National Financial Educators Council 2022 Survey.

iii IRI Retirement Readiness Research Series: “Retirement Readiness Among Older Workers 2021” (August 2021).

iv “Retirement Insecurity 2021” The National Institute of Retirement Security (February 2021).

v Internal Revenue Service release, Nov. 1, 2023. https://www.irs.gov/newsroom/401k-limit-increases-to-23000-for-2024-ira-limit-rises-to-7000

vi IRA Financial, “Solo 401(k) Contribution Limits,” Jan. 2, 2024.

vii For example, those found on Bankrate.com, Schwab.com, Fidelity.com, etc.

viii The American College of Trust and Estate Counsel: “State Death Tax Chart,” January 2022.