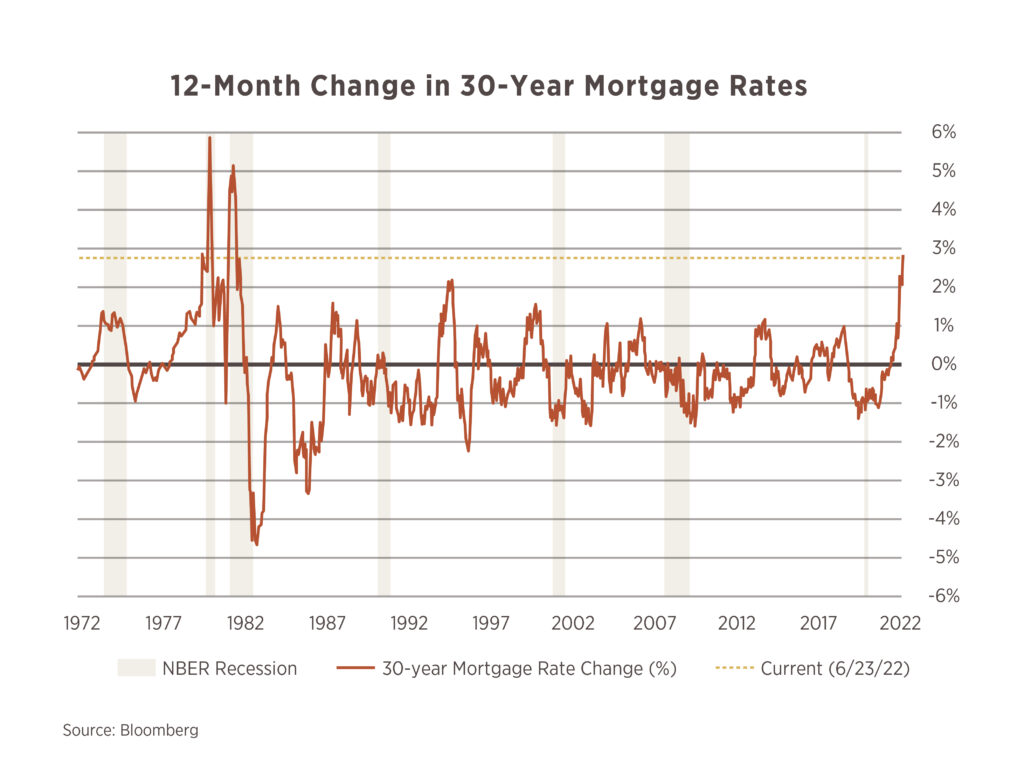

Chart of the Month

We recently discussed inflation and its driving forces. Housing appreciation is providing tailwinds to the inflation narrative, but as the Fed has embarked on a fast rate hiking cycle, what is happening to the affordability of the housing sector? This month’s chart shows that 30-year mortgage rates have nearly doubled to 5.8% compared to last year’s rate of 3%. This rate of increase hasn’t been seen since the early 1980s. What does this mean for a monthly payment?

The median home sale price in the US is $410,000 with a median down payment of 12%. The monthly payment on a 30-year mortgage at 5.8% would be $2,100. A year ago, that same house was likely only $355,000 given the appreciation in home prices over the past 12 months of 15%(1). Incorporating the lower sale price and the lower mortgage rates, the same house bought one year ago would have had a monthly payment of $1,300, $800 less than today! This will likely begin to cool housing demand and allow the supply of homes to catch up. This is part of the Federal Reserve’s playbook to slow the economy down so inflation starts to moderate.

(1) National Association of Realtors (May 2022)

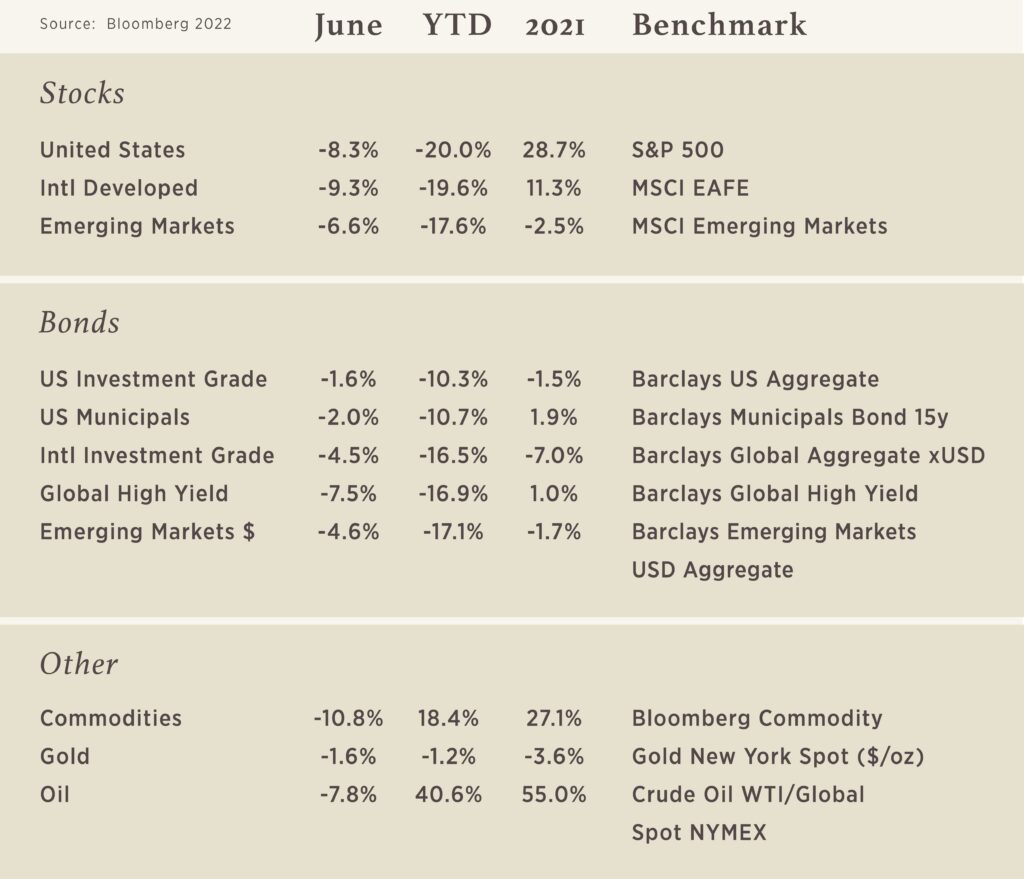

Recent market volatility has been unsettling. Watching markets and account values fall can unnerve even the most sophisticated, professional investor. But with challenge comes opportunity. With a focus on the long term and with an opportunistic mindset, you can stay disciplined and focused on taking action in areas you can control.

Here are a few examples of resulting strategies:

Tax-loss harvesting

Now may be a good time to consider or accelerate plans to harvest losses — the practice of selling investments trading at a loss, replacing them with similar assets, and then offsetting gains with those losses. After capital gains and capital losses are netted against one another, any remaining net capital loss may be used to offset ordinary income up to $3,000 per year. Furthermore, unused net capital losses may be carried over in unlimited amounts and used against future gains and income until exhausted. This means that even if you haven’t realized any gains yet this year, there may still be benefits to harvesting losses — rather than waiting, as is commonly the case, until closer to year end.(1)

Investing cash reserves

If you currently have excess cash on your balance sheet, now may offer a good opportunity to put a portion of it to work. But keep in mind, there is no crystal ball in forecasting future market returns. Prices could fall further, which is one reason why taking a measured approach, deploying only a portion of your cash and keeping the rest for “dry power”, may be the more prudent approach. Either way, prepare for the possibility that you could invest your cash today in assets that fall significantly in value tomorrow, the next day or the next week. And that wouldn’t mean you necessarily made the wrong choice. This strategy is not the same as market timing. It is about taking advantage of volatility to bring your allocation in line with the overall risk profile best suited for your long-term goals.

Converting to a Roth IRA

Owners of traditional IRAs may convert them into Roth IRAs. Roth IRAs are unique in that you may not deduct contributions made to them from income, but may take qualifying distributions free of federal income tax (assuming certain requirements are met).

A Roth conversion requires a distribution from your traditional IRA that is subject to federal income tax. But in the conversion process, if you are under age 59½, you are not subject to the 10% tax on premature distributions from traditional IRAs. However, if you subsequently take a distribution from the Roth IRA within five years of the conversion date, then a 10% penalty tax applies.

If you have been considering a Roth conversion, now may be an opportune time to act, because completing one at depressed market values lessens the tax liability from the conversion and effectively allows you to buy securities within the Roth IRA at much lower values, with the opportunity to capture subsequent appreciation. And this doesn’t need to be an all or nothing strategy. You could, for example, convert half now and then a remaining portion several months from now as you continue to watch market performance.

However, please note that the conversion could put you in a higher income tax bracket, so you will want to work closely with your advisors to understand the overall tax implications.

Taking advantage of estate planning opportunities such as grantor-retained annuity trusts. (GRAT)

If you plan to transfer significant wealth to your family, and especially if you expect your taxable estate to be above federal and/or state estate tax exemption levels, you may want to consider estate planning opportunities that become more attractive during down markets.

One example is a funding a GRAT, or if you already have a GRAT with the power of substitution, swapping assets in your GRAT. GRATs allow you to transfer assets to a trust in exchange for annuity payments for a set period of years. If structured properly, at the end of the term, any appreciation above the IRS-mandated 7520 interest rate (the hurdle rate) passes to beneficiaries free of tax. While the 7520 interest rate has risen considerably in recent months, it is still a relatively low hurdle to clear should equity markets rebound significantly within the next couple of years.

Another example is gifting securities to your beneficiaries. Instead of transferring cash to take advantage of the annual gift tax exclusion ($16,000 per person in 2022) or lifetime estate tax exclusion ($12.06 million per person in 2022 but set to be cut in half in 2026), you could gift stocks or other securities that have fallen in value. Assuming they appreciate in future years, this allows you to transfer more assets out of your taxable estate.

Additional examples include charitable lead annuity trusts, intrafamily transactions and installment sales to intentionally defective grantor trusts — all which may allow you to transfer assets out of your taxable estate in a more efficient manner if executed at lower asset values.

The above strategies are simply examples and are certainly not appropriate for all investors. To assess whether they may be right for you, and to uncover more ideas for navigating the current market environment, please reach out to your advisor.

(1) Internal Revenue Service. “Topic No. 409 Capital Gains and Losses,” retrieved from https://www.irs.gov/taxtopics/tc409 on May 23, 2022. (1) US Securities and Exchange Commission.” “Wash Sales.” Retrieved from https://www.investor.gov/introduction-investing/investing-basics/glossary/wash-sales on May 23, 2022.

All videos were recorded on May 12, 2022