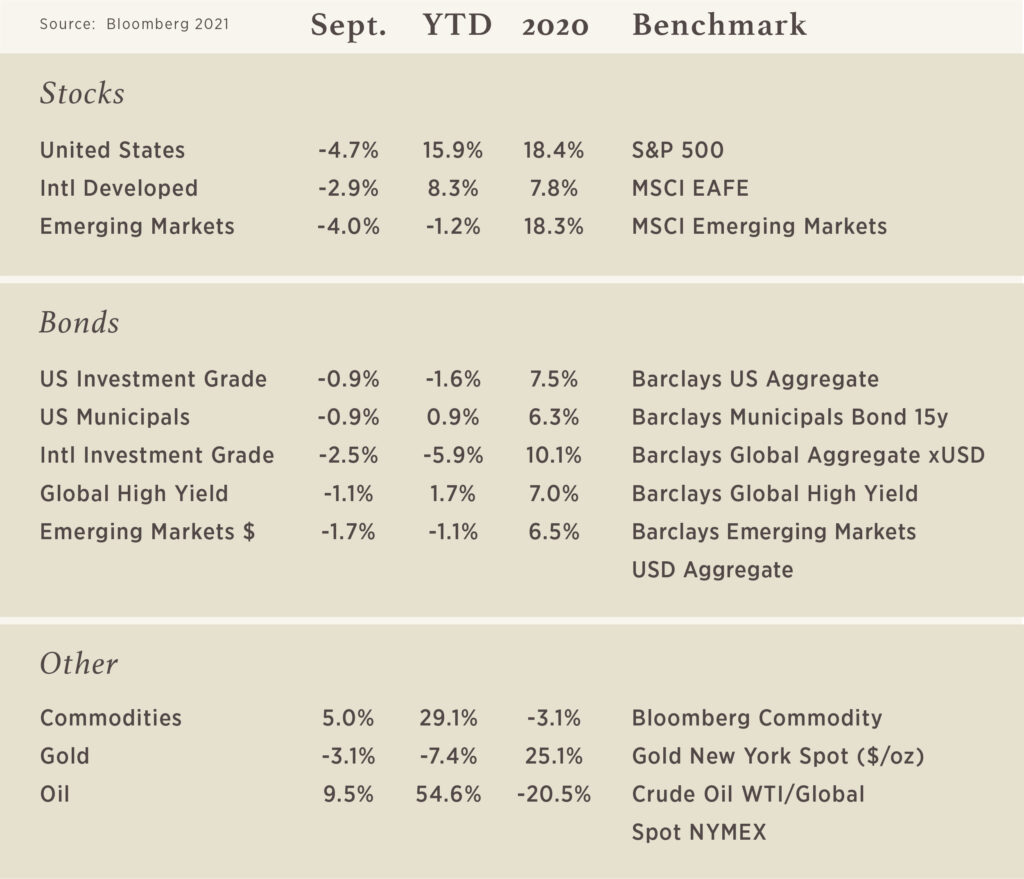

Chart of the Month

It has never been cheaper to finance a new house, a new car or just about anything you can borrow against (including stocks). The chart above shows the Goldman Sachs Financial Conditions Index with data back to 1983. We currently are at the lowest levels ever. These easy financial conditions encourage spending and speculative activity and are likely a contributing factor to the strong performance of the stock market. Despite this indicator painting a rosy picture for robust growth in the US in the immediate future, it is likely to be supportive of policymakers paring back on their stimulus that provided a much-needed spark at the onset of the pandemic.

If you have a child with special needs, a trust may be a financial priority.

There are many crucial goods and services that Medicaid and Supplemental Security Income might not pay for, and a special needs trust may be used to address those financial challenges. Most importantly, a special needs trust may help provide for your disabled child in case you’re no longer able to care for them.

Remember, using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

In preparing for a special needs trust, one of the most pressing questions is: when it comes to funding the trust, what are the choices?

There are four basic ways to build up a third-party special needs trust.

One method is simply to pour in personal assets, perhaps from immediate or extended family members. Another possibility is to fund the trust with life insurance. Proceeds from a settlement or lawsuit can also serve as the core of the trust assets. Lastly, an inheritance can provide the financial footing to start and fund this kind of trust.

Families choosing the personal asset route may put a few thousand dollars of cash or other assets into the trust to start, with the intention that the initial investment will be augmented by later contributions from grandparents, siblings, or other relatives. Those subsequent contributions can be willed to the trust, or the trust may be named as a beneficiary of a retirement or investment account.1,2,3

When life insurance is used, the trustor makes the trust the beneficiary of the policy. When the trustor dies, the policy’s death benefit is left to the trust.1,2,4

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

A lump-sum settlement or inheritance can be invested while within the trust. With a worthy trustee in place, there is less likelihood of mismanagement, and funds may come out of the trust to support the beneficiary in a measured way that does not risk threatening government benefits.

Care must be taken not only in the setup of a special needs trust, but in the management of it as well. This should be a team effort. The family members involved should seek out legal and financial professionals who are well versed in this field, and the resulting trust should be a product of close collaboration.