After building enough income to live comfortably, young adults may find themselves looking for the next step in solidifying their financial future. 73% of Americans aged 18-25 reported having a savings account, while 27% reported owning stock, and only 11% reported owning mutual funds.1 If you’ve received money from family, have funds from your 529 plan leftover, or you received a pay raise at work, you should be asking yourself whether it’s time to save, invest, or do both.

Choosing to save or invest can be a challenging decision for individuals as the choice often depends on their financial goals. Both saving and investing are great options to accumulate money. Saving earns a lower return but has virtually no risk, while investing can earn a higher return but there is a risk of loss. So, which is the right one to do? Here are some tips to figure out which method is best for you, including the advantages and disadvantages of both methods.

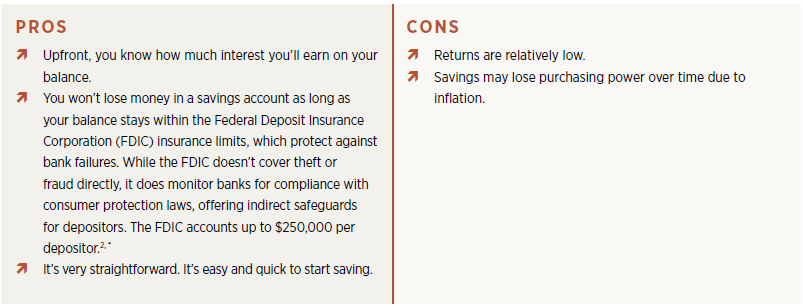

Saving is the process of putting money aside gradually. It provides a safety net as it enables you to set aside money for emergencies, short-term goals, or unexpected expenses. Building a savings habit can offer a sense of stability and financial flexibility, especially in uncertain economic times. While it may not offer high returns like investing, saving is about security and stability. Below are some of the benefits and drawbacks of saving.

Saving: Overview, Pros, Cons, and Tips

Saving is the process of gradually setting aside money. It provides a financial safety net for emergencies, short-term goals, or unexpected expenses. While it may not offer high returns, saving is about security and stability.

Investing: Overview, Pros, and Cons

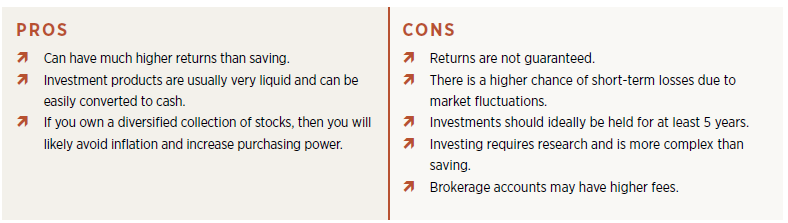

Investing involves purchasing assets with the potential to grow in value or generate higher returns, such as stocks, bonds, or real estate. It can help outpace inflation and build long-term wealth, though it comes with risk.

Tips for Investing

Consider the following strategies to make the most of your investments:

- Don’t be afraid of aggressive asset allocation. Although there is a higher risk, there is more time to make up for losses. Over longer periods of time, aggressive investment portfolios outpace conservative ones.3

- Be tax aware. Consider your tax rate and how investment accounts are taxed.

- Investing gives your money the potential to grow and work with you over time. While it comes with risks, investing also offers opportunities that saving alone can’t provide. With the right research and a long-term perspective, investing can be a powerful way to build wealth and achieve future milestones.

Conclusion

Overall, saving is better if you need the money within the next few years. Investing is more suitable if you don’t need the money for at least 5 years and are comfortable with risk. Regardless of your choice, it is good practice to keep enough money in your checking account to cover a month’s worth of bills and maintain 3–6 months of expenses in your savings for emergencies. After that, you should prioritize saving for retirement.

Start building a stronger retirement today. By investing early, you can take full advantage of compound growth and reduce the amount you need to save each year. Let us help you choose the right path to help reach your financial goals. Contact us now to get started.

1. Data sheet: Young adult financial well-being. Asset Funders Network. (2023, May 5). https://assetfunders.org/resource/data-sheet-young-adult-financial-well-being/

2. Deposit Insurance FAQs | FDIC.gov. (n.d.). Retrieved July 1, 2025, from https://www.fdic.gov/resources/deposit-insurance/faq

3. https://www.schwab.com/learn/story/is-it-time-to-reassess-your-risk-tolerance

*Note: Before opening a savings account, you should confirm whether the institution you are depositing into is FDIC-insured, as not all institutions are.