Storing your legal and financial documents efficiently can help you prepare to meet life’s challenges—from paying bills to filing taxes, enrolling a child in school to estate planning, and everything in between. Understanding what you can discard, which papers you should hold onto (and for how long), and how to organize it all can save you time, energy, and space.

How To Get Started

Gather and separate your documents: Begin by gathering all your papers together. Walk through each room in your home, collecting any loose paper. Pay special attention to frequently used “drop areas” where things accumulate: an entryway table, mudroom storage cubbies, kitchen counters, junk drawers, desks, and nightstands. Look through your purse, laptop bag, and your children’s backpacks.

Once you’ve pulled everything together, separate your collection into three piles: important (to keep), unnecessary/sensitive (to be shredded), and unnecessary/general (to be discarded). If you don’t need a document but it contains personal or sensitive information, set it aside to shred later. General papers such as junk mail, catalogs, magazines, bill inserts, empty envelopes, and outdated school communications can simply be thrown away or recycled.

Now, you can decide which document organization system will work best for you.

Create Your Filing System

Consider what filing systems you may need to create. Think about how you want to access your financial records in the short term, as well as how to store them for years to come.

Physical files

- A binder might work well for a single person to house paper records.

- A file drawer or cabinet might be a better option for a larger family or business owner.

- An at-home fireproof lockbox or safe can be a good choice to store important legal documents if you need to access them regularly (such as copies of your will, birth certificates, and passports).

- A safe deposit box at your bank can be a good option for storing hard-to-replace documents (such as contracts, military discharge papers, house deeds and car titles, and physical stock and bond certificates). You can also use it to store small valuables like jewelry, collectibles or family heirlooms.

Digital files

In addition to keeping physical files of important documents, you may want to store copies of them electronically. Make sure to save these digital files not just to a local computer hard drive—which can crash or break—but also to a secure, encrypted cloud storage service. Your financial advisor may offer you access to an online client portal, which can also be used to store important documents.

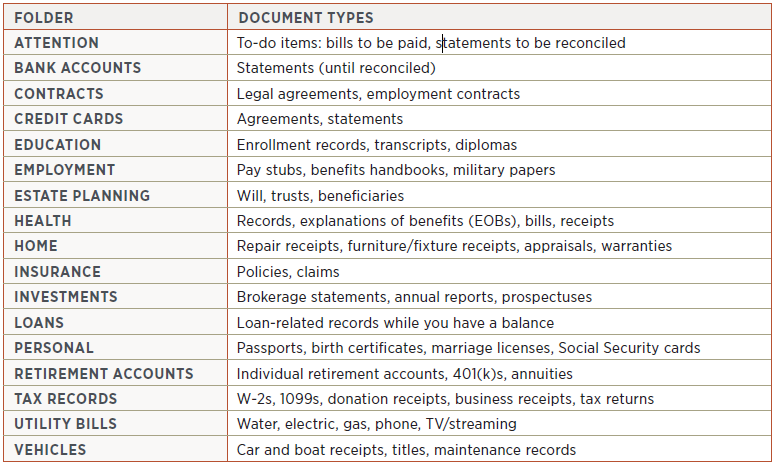

Next, develop a filing system that makes sense to you. Label your folders using easy-to-remember terms. For example:

Within each of these folders, organize your documents chronologically. This will help you access the latest versions and make it easier to remove out-of-date ones.

How Long To Keep Your Financial Documents

Less than one year: ATM, bank deposit, and credit card receipts. Once you’ve reconciled them with your monthly statements, you can shred these paper documents or securely trash electronic files unless you need them to support your tax return. Keep insurance policies and investment statements until new ones arrive.

One year or more: Hold onto loan documents until the loan is paid off (often more than one year). If you own a car, keep the title until you sell it. If you own investments such as stocks, bonds, and mutual funds, keep your purchase confirmations until you sell so that you can establish your cost basis and holding period.

Seven years: If you fail to report your gross income on your tax returns, the government has six years to collect the tax or start legal proceedings. Therefore, keeping all your tax records for at least seven years is a good idea.

Forever: Keep crucial records such as birth and death certificates, marriage licenses, divorce decrees, Social Security cards, and military discharge papers indefinitely. You should also hold onto any defined benefit plan documents, estate planning documents, life insurance policies, and an inventory of what’s inside safe deposit boxes.

PRO TIP: Tackle this project in phases

Here are some good rules of thumb for how long to hold onto documents:

- Take small steps. Don’t try to organize your life and declutter your home in one sitting. If needed, divide the organizational tasks we’ve described across multiple days. For example, on Day 1, collect and sort your papers (keep, discard, shred). On Day 2, establish a filing system and select your storage methods. On Day 3, sort and file the important documents you’ve chosen to keep.

- Create an inbox. Designate a place in your home that will serve as an “inbox” to collect your mail, bills, receipts, and important documents when they arrive. Schedule time to sort through your inbox on a frequent, regular basis (daily or weekly). File the papers you wish to keep using the system you’ve created. Discard or destroy papers you do not need to store using secure methods.

- Assess your system. After a few months (and eventually, on an annual basis), sift through your paper files and electronic records and remove outdated ones. Review your filing system to see whether it is working for you or if any changes need to be made—such as adding a new folder or reorganizing your electronic files. Archive any records (such as old tax returns) that you’d like to retain but do not need to be in your immediate filing system. Review the contents of your safe deposit box to ensure you know what is stored there.

With a few simple steps, you can establish an organizational system that safeguards your important documents while allowing you to access them when needed. If you have any questions regarding what types of documents you should retain or for how long, please contact a member of our team.