In recent years, such headlines about Roth IRAs have become commonplace, stemming from the prospect of increasing tax rates and the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act) and the subsequent SECURE 2.0 Act passed in 2022.

But what exactly is a Roth IRA? Who should have one? And is it worth taking the time to find out—especially if you already have retirement accounts?

In short, the answer is yes. While Roth IRAs aren’t for everyone—nor is everyone eligible to contribute to one—the potential tax savings associated with them, and other key benefits, can make a meaningful difference in one of the most important financial journeys one can take: preparing for retirement.

Here is some baseline information about Roth IRAs to help you begin considering whether one might be right for you.

What does “Roth” stand for?

Roth IRAs are named after former Delaware Senator William V. Roth, Jr., who was instrumental in legislation passed into law in 1997 that established the account type—allowing individuals to invest after-tax income into IRAs that can be withdrawn tax-free in retirement. Senator Roth served 34 years in Congress, during which he chaired the Senate Finance Committee, the Governmental Affairs Committee and the Permanent Subcommittee on Investigations.1

What is a Roth IRA?

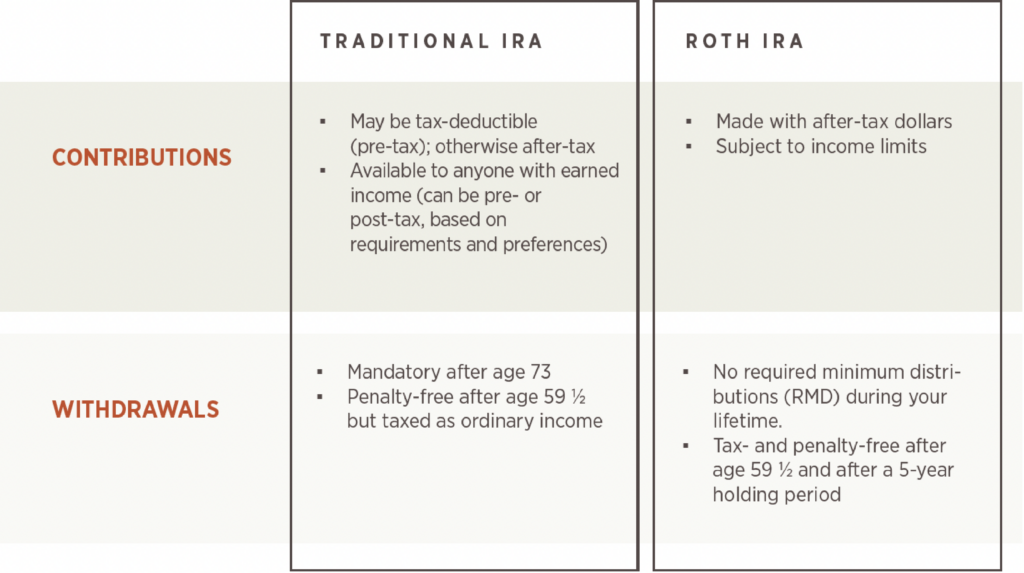

A Roth IRA is a retirement savings vehicle that differs from most retirement savings accounts in that contributions are made with after-tax dollars, and withdrawals are tax exempt, assuming certain requirements are met. The inverse is generally true for traditional IRAs: qualified contributions are tax deductible, but withdrawals count towards taxable income.

How else do Roth IRAs differ from traditional IRAs?

Other main differences include the following:

- Required minimum distributions (RMDs) are generally not required from Roth IRAs during the original owner’s lifetime

- Penalty-free withdrawals can be made under a wider set of circumstances, including if they:

- Come from contributions you have made rather than earnings on your contributions

- Were made because you are disabled

- Were made to a beneficiary or to your estate after your death

- Were made to buy or rebuild a first home, subject to various Internal Revenue Service (IRS) requirements

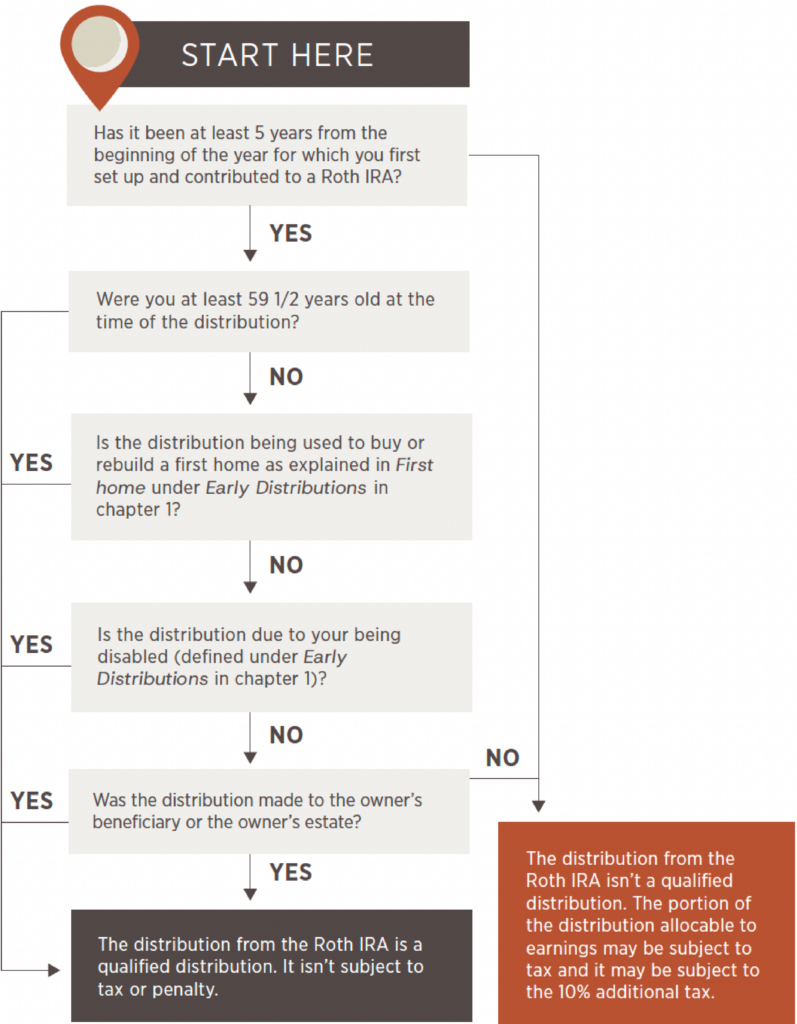

IRS flowchart

The below flowchart provides information from the IRS Publication 590-B to help you determine if a distribution from a Roth IRA would be tax and penalty free. Refer to chapters 1 and 2 of the publication for further clarification.

Is the distribution from your Roth IRA a Qualified Distribution?

Source: Internal Revenue Service. “Publication 590-B (2021), Distributions from Individual Retirement Arrangements (IRAs),” retrieved from https://www.irs.gov/publications/p590b#en_US_2021_pub-link100089542. Updated April 5, 2023.

Can anyone own a Roth IRA?

Anyone can own a Roth IRA, but only taxpayers below certain income thresholds can contribute to one. In 2026, the threshold for single taxpayers is $153,000 with a contribution phase-out beginning at $168,000, and the threshold for joint filers is $242,000 with a contribution phase-out beginning at $252,000.

The following chart from the IRS summarizes this eligibility criteria:

2026 Roth & Traditional IRA Income & deduction Limits TIAA | TIAA. (n.d.). Retrieved March 19, 2026, from https://www.tiaa.org/public/retire/financial-products/iras/ira-contributions-tax-benefits/income-and-deduction-limits

How much can you contribute to a Roth IRA?

For 2026, the total contributions you make to all of your traditional Roth IRAs can’t be more than:

- $7,500 ($8,600 if you’re age 50 or older)2, or

- If less, your taxable compensation for the year

You can contribute to a Roth IRA, if you otherwise are eligible, even if you participate in another retirement plan through your employer or business. You (or your spouse) can also set up and contribute to a Roth IRA if your spouse (or you) is not working (or working part-time), based on the earnings of the working spouse. This type of IRA is often called a “spousal IRA.” This means that, based on 2026 contribution limits, you could contribute a total of $15,000 ($17,200 if you’re age 50 or older) as a couple.

Why would someone choose a Roth IRA over a traditional IRA?

The main reason you might decide to contribute to a Roth IRA instead of a traditional IRA is if you expect your taxable income to be higher in retirement than it is now. If that is the case, taking the tax hit now (rather than when you make withdrawals in retirement) while at a lower tax rate could make sense.

Another reason a Roth IRA may be preferred is if you expect to transfer your retirement assets to your heirs rather than spend it. In most cases, beneficiaries of Roth IRAs can make tax-free withdrawals from a Roth IRA over 10 years.

There may be other reasons for establishing or converting to a Roth IRA, including if you expect income taxes more generally to rise in future years. In any case, your financial advisor and accountant can help you determine if you are a good candidate.

What is a Roth conversion?

If you own a traditional IRA, you can convert it into a Roth IRA. The amount converted is generally subject to federal income tax in the year of the conversion. However, if you are under the age of 59 ½ and take a distribution of the converted amount within five years of the conversion, a 10% penalty tax may apply unless an exception applies. Distributions taken after age 59 ½ are not subject to this penalty.

Examples of favorable conversion scenarios include:

- When your income and taxes are relatively low, for example, in retirement

- During stressed markets when asset values are lower, lessening the tax liability from the conversion and allowing you to buy securities within the Roth IRA at much lower values, with the opportunity to capture subsequent appreciation

- When you have determined you have sufficient assets to fund your retirement without making withdrawals from your retirement accounts (which become mandatory at age 73 based on your birth year, for a traditional IRA)

What is a “backdoor” Roth?

As previously described, under current law, taxpayers with income (in 2026) of at least $168,000 ($252,000 if married) are prohibited from contributing to a Roth IRA. “Backdoor” and “mega backdoor” Roth contributions are strategies that allow high earners to participate in Roth accounts nonetheless.

A “backdoor” Roth contribution strategy works as follows:

- Although higher earners (as defined above) are barred from contributing to a Roth IRA, they are allowed to convert traditional IRA assets into a Roth IRA.

- When converting traditional IRA assets into a Roth IRA, taxpayers owe tax on the gains that have accrued from their contributions.

- To minimize taxes, some taxpayers make after-tax contributions to a traditional IRA and then convert those funds to a Roth IRA shortly thereafter, limiting the amount of taxable gain.

This strategy is generally most effective for individuals who do not already have significant pre-tax balances in traditional, SEP, or SIMPLE IRAs. If pre-tax IRA assets are present, the IRS requires that conversions be treated as coming proportionally from both pre-tax and after-tax dollars, which can result in a portion of the conversion being taxable.

There is also a “mega backdoor” conversion strategy applicable to workers who have employer-sponsored retirement plans that allow after-tax contributions and after-tax conversions to a Roth 401(k). If both these features are offered, participants can take full advantage of the $72,000 annual retirement savings plan contribution limit in 20263 (for both employee and employer contributions) by making after-tax contributions, and then converting those contributions to a Roth 401(k).

Under previously proposed changes to tax law, these backdoor strategies would no longer be viable. While these proposals ultimately did not become law, it is still possible that they are revisited by legislators in the future.

Finally, investors should be aware of the IRA aggregation rule, which treats all traditional IRAs as a single account for tax purposes. This rule can affect the taxation of a conversion, so it is important to review your specific situation with a financial advisor before proceeding.

How can I decide if a Roth IRA is right for me?

Deciding between a Roth IRA and traditional IRA can be difficult without perfect foresight into the future. And sometimes the answer is “both.” Likewise, deciding if, when and how to convert to a Roth IRA or make the most of a “backdoor” strategy can be even more complicated.

To help guide your decision, please reach out to us. We can coordinate with your accountant to make a well-informed decision and streamline the process.

1. Delaware Historical Society. (2022, October 11). Biography – Senator William V Roth – Delaware Historical Society. https://dehistory.org/collections/about-our-collections/senator-william-v-roth-collection/biography/

2. Roth IRA income and contribution limits for 2026. Vanguard. (n.d.). https://investor.vanguard.com/investor-resources-education/iras/roth-ira-income-limits. Accessed 19 Mar. 2026.

3. Roth 401(k) contribution limits for 2025 and 2026. (2025, December 19). Fidelity. https://www.fidelity.com/learning-center/smart-money/roth-401k-contribution-limits